Credit History and Car Insurance: Understanding the Connection

How Your Credit Score Impacts Car Insurance Rates Credit Score and Insurance Premiums

Okay, let's talk about something that might not be immediately obvious: your credit score and how it affects what you pay for car insurance. You're probably thinking, "Wait a minute, what does borrowing money have to do with my driving?" Well, insurance companies use credit scores as one factor to predict how likely you are to file a claim. They figure that people who manage their finances responsibly are also more likely to be responsible drivers. Sounds a bit unfair, right? But that's how the system works in many states.

Think of it this way: insurance companies are all about risk assessment. They're trying to figure out how much of a risk you are to insure. A good credit score suggests that you're reliable and predictable, which translates to a lower risk in their eyes. A poor credit score, on the other hand, might signal that you're less reliable, and they might charge you more to cover the perceived higher risk. It's like they're saying, "Hey, you're a bit of a gamble, so we need to charge you more just in case."

This isn't just some wild theory. Studies have actually shown a correlation between credit scores and insurance claims. People with lower credit scores tend to file more claims, and those claims tend to be more expensive. So, even though it seems unrelated, your credit history really can impact your car insurance rates. It's all about the numbers and the probabilities for these insurance companies.

Decoding Credit Scores Understanding Different Credit Score Ranges for Car Insurance

So, what exactly is a "good" credit score when it comes to car insurance? Well, it depends on the scoring model the insurance company uses, but generally, the higher your score, the better. Credit scores typically range from 300 to 850. Here's a rough breakdown:

- Excellent (750-850): You're in great shape! You'll likely qualify for the best insurance rates.

- Good (700-749): Still pretty good. You should get decent rates, though not the absolute lowest.

- Fair (650-699): This is where things start to get a little tricky. You might see higher rates than those with good or excellent credit.

- Poor (550-649): Expect to pay significantly more for car insurance. You might want to shop around for the best deals.

- Very Poor (300-549): You'll likely face the highest insurance rates. You may even have trouble finding an insurer willing to cover you.

Keep in mind that these are just general guidelines. Each insurance company has its own criteria, and the impact of your credit score can vary depending on the state you live in. Some states actually prohibit insurance companies from using credit scores to determine insurance rates. So, do your research and find out what the rules are in your area.

Improving Your Credit Score for Lower Car Insurance Premiums Credit Repair Strategies

Okay, so you're not happy with your credit score and its impact on your car insurance rates. What can you do about it? The good news is that you can improve your credit score over time. Here are some strategies:

- Pay your bills on time: This is the single most important thing you can do. Payment history makes up a large portion of your credit score.

- Keep your credit utilization low: Don't max out your credit cards. Aim to use less than 30% of your available credit.

- Check your credit report regularly: Look for errors or inaccuracies that could be dragging down your score. You're entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year.

- Don't open too many new credit accounts at once: Opening multiple accounts in a short period of time can lower your average account age and make you look riskier to lenders.

- Consider a secured credit card: If you have poor credit, a secured credit card can be a good way to rebuild your credit. You'll need to put down a deposit, which will serve as your credit limit.

Improving your credit score takes time and effort, but it's definitely worth it. Not only will you save money on car insurance, but you'll also benefit from lower interest rates on loans and credit cards.

Car Insurance Companies and Credit Checks Understanding Insurance Company Credit Inquiries

When you apply for car insurance, the insurance company will likely check your credit report. This is usually a "soft inquiry," which means it won't affect your credit score. However, it's still important to understand what they're looking for.

The insurance company will use your credit report to assess your risk level. They'll look at your payment history, credit utilization, and overall creditworthiness. They may also consider factors like bankruptcies or foreclosures.

If you're concerned about the impact of credit checks on your credit score, you can ask the insurance company whether they use a "soft inquiry" or a "hard inquiry." A hard inquiry can slightly lower your credit score, but it's usually a small and temporary effect.

States Where Credit Scores Don't Affect Car Insurance Rates Credit Score Ban States

As mentioned earlier, some states prohibit insurance companies from using credit scores to determine insurance rates. These states include:

- California

- Hawaii

- Massachusetts

- Michigan (limited use)

If you live in one of these states, your credit score won't be a factor in your car insurance rates. However, insurance companies can still consider other factors, such as your driving record, age, and the type of car you drive.

Alternative Car Insurance Options for Drivers with Bad Credit High-Risk Insurance and Usage-Based Insurance

If you have bad credit and are struggling to find affordable car insurance, there are a few alternative options you can consider:

- High-risk insurance: Some insurance companies specialize in insuring drivers with bad credit or a poor driving record. These policies tend to be more expensive than standard insurance, but they can provide coverage when other options are limited.

- Usage-based insurance: This type of insurance uses telematics devices to track your driving habits. Your rates are based on how you actually drive, rather than your credit score. If you're a safe driver, you could save money with usage-based insurance.

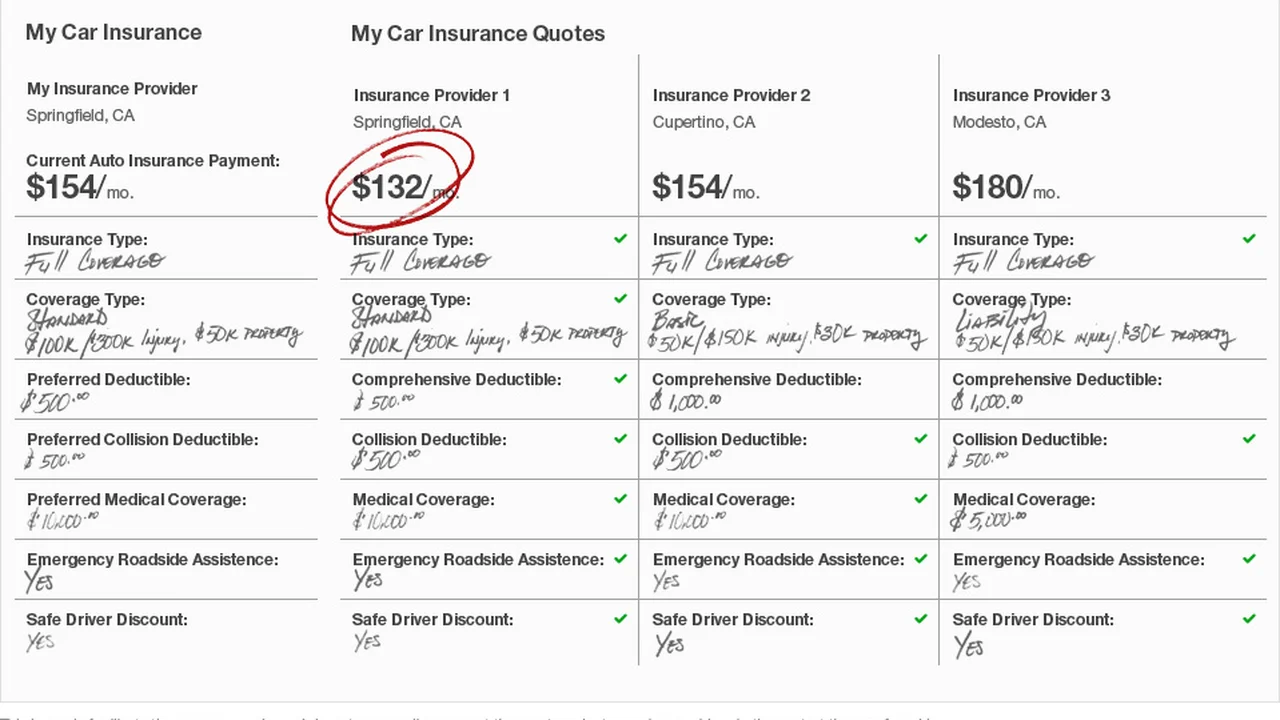

- Shop around: Don't settle for the first quote you get. Shop around and compare rates from multiple insurance companies. You might be surprised at the differences in prices.

Comparing Car Insurance Products for Different Credit Profiles Recommendations and Pricing

Let's look at some specific car insurance products and how they might fit different credit profiles. Remember that prices can vary wildly based on location, driving history, and coverage levels, so these are just examples.

For Drivers with Excellent Credit (750+)

You're in a great position! You can likely qualify for the best rates and coverage options from almost any major insurer. Consider these options:

- State Farm: Known for excellent customer service and a wide range of coverage options. A policy with full coverage (liability, collision, and comprehensive) for a driver with an excellent credit score and clean driving record in a suburban area might cost around $1200 - $1500 per year.

- GEICO: Aggressive pricing and easy online quote process. Similar coverage as State Farm might be around $1100 - $1400 per year.

- USAA (for military members and their families): Consistently ranked highly for customer satisfaction and competitive rates. Their rates are often the best, but eligibility is limited.

Usage Scenario: These insurers provide peace of mind with comprehensive coverage and reliable claims processing. They are suitable for daily commuters, families, and anyone who wants the best protection available.

For Drivers with Fair to Poor Credit (600-699)

You'll need to shop around more aggressively. Some insurers are more forgiving of lower credit scores than others. Consider these options:

- Progressive: Known for insuring higher-risk drivers. Their rates will likely be higher than State Farm or GEICO for someone with excellent credit, but they might be competitive for someone with fair credit. Expect to pay $1800 - $2500 per year for similar full coverage.

- The General: Specifically targets drivers with less-than-perfect credit and driving records. Their rates will likely be higher than Progressive, but they can provide coverage when other insurers won't. Expect to pay $2200 - $3000+ per year.

- Direct Auto Insurance: Similar to The General, focusing on high-risk drivers.

Usage Scenario: These insurers offer coverage to those who might be denied by other companies. They are suitable for drivers who need to get back on the road quickly and are willing to pay a premium.

Usage-Based Insurance Options

Regardless of your credit score, usage-based insurance can be a good way to save money if you're a safe driver.

- Progressive Snapshot: Tracks your driving habits (hard braking, speeding, nighttime driving) and offers discounts for safe driving.

- Allstate Drivewise: Similar to Progressive Snapshot.

- State Farm Drive Safe & Save: Also tracks driving habits for potential discounts.

Usage Scenario: These programs are ideal for drivers who are confident in their safe driving skills and are willing to share their driving data in exchange for potential savings.

Product Comparison: A Quick Glance

| Insurer | Credit Score Focus | Coverage Options | Approximate Annual Premium (Full Coverage, Suburban Area) | Key Features |

|---|---|---|---|---|

| State Farm | Excellent | Comprehensive | $1200 - $1500 | Excellent customer service, wide range of coverage |

| GEICO | Excellent | Comprehensive | $1100 - $1400 | Competitive pricing, easy online quote |

| Progressive | Fair to Poor | Comprehensive | $1800 - $2500 | Insures higher-risk drivers, Snapshot program |

| The General | Poor | Basic to Comprehensive | $2200 - $3000+ | Specializes in high-risk drivers |

Important Note: These prices are estimates only. Always get a personalized quote from each insurer to determine the actual cost of coverage. Remember to compare coverage levels and deductibles as well as price.

Understanding Car Insurance Deductibles and Credit Score Influence Deductible Options and Cost Savings

Your deductible – the amount you pay out-of-pocket before your insurance covers the rest – can also indirectly be affected by your credit score. While your credit score doesn't directly change the deductible options available, it *does* affect your overall premium. And that can influence your decision on which deductible to choose.

Here's how:

- Lower Credit Score = Higher Premium: If you have a lower credit score, you're already paying a higher premium. This might make you hesitant to choose a lower deductible (which would increase your premium even further). You might opt for a higher deductible to keep your monthly costs down, even though it means paying more out-of-pocket if you have an accident.

- Higher Credit Score = Lower Premium: If you have a good credit score, you're paying a lower premium. This gives you more flexibility to choose a lower deductible without significantly impacting your monthly costs. You can have the peace of mind of knowing you'll pay less out-of-pocket in case of an accident.

Example: Let's say you have a fair credit score and are quoted $2000 per year for car insurance with a $500 deductible. Lowering your deductible to $250 might increase your premium by $300 per year, bringing the total to $2300. You might decide that the extra $300 per year isn't worth the $250 reduction in your deductible, especially if you're on a tight budget.

However, if you have an excellent credit score and are quoted $1200 per year with a $500 deductible, the same $300 increase might be more palatable. You're still paying less than someone with a fair credit score, even with the lower deductible.

The Role of Credit History in Car Insurance Claims Handling Claim Processing and Creditworthiness

While your credit score shouldn't directly affect *whether* your claim is approved, it *can* indirectly impact the claims handling process. Insurance companies are businesses, and they're always looking for ways to minimize their risk.

Here's how your credit history might play a subtle role:

- Perceived Risk: If you have a history of financial instability (as reflected in your credit report), the insurance company might be more cautious about verifying the details of your claim. They might scrutinize the information you provide more closely and take longer to process your claim. This isn't necessarily fair, but it's a reality of the business.

- Potential for Fraud: In extreme cases, a very poor credit history might raise red flags about the potential for insurance fraud. The insurance company might be more likely to investigate the claim thoroughly to ensure it's legitimate.

It's important to emphasize that insurance companies are obligated to handle all claims fairly and in good faith, regardless of the claimant's credit history. However, the perceived risk associated with a poor credit score can sometimes lead to a more cautious and thorough claims process.

Future Trends in Car Insurance Pricing The Evolving Landscape of Credit and Insurance

The relationship between credit scores and car insurance rates is constantly evolving. There's growing debate about the fairness of using credit scores to determine insurance premiums, and some states are pushing for reforms.

Here are some potential future trends:

- Increased Regulation: More states might follow the lead of California, Hawaii, and Massachusetts in banning the use of credit scores for car insurance pricing.

- Greater Transparency: Insurance companies might be required to be more transparent about how they use credit scores and other factors to determine rates.

- Alternative Risk Assessment Models: Insurers might develop alternative risk assessment models that rely less on credit scores and more on factors like driving history, telematics data, and other behavioral indicators.

- Personalized Insurance Products: We might see more personalized insurance products that are tailored to individual driving habits and risk profiles, rather than relying on broad generalizations based on credit scores.

The future of car insurance pricing is uncertain, but it's likely that the role of credit scores will continue to be debated and challenged in the years to come.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)